CBDCs Branded as Closing Orwell’s ‘1984 Loop’

Central Bank Digital Currencies are in the spotlight. Supporters see faster payments and policy tools. Critics warn that programmable money could enable full oversight of how people earn, save, and spend. When people say CBDCs are “closing the 1984 loop,” they mean the technology could let authorities track every transaction and add rules to your money. This article explains the claim, how CBDCs actually work, where projects stand, and what skills you need to stay ready.

If you want a solid foundation before you form a view, consider a Crypto Certification. Learning the mechanics behind digital money will help you evaluate the risks and the opportunities with confidence.

What “closing the 1984 loop” really means

The phrase comes from privacy advocates who fear CBDCs could combine the reach of central banks with detailed payment data. They point to two features. First is traceability. Every transfer can be logged. Second is programmability. Money can carry rules. Examples include spending limits, time-bound vouchers, or targeted stimulus. Critics argue this mix could let institutions monitor behavior and steer it through payment rails. Supporters reply that any national system would include strict legal safeguards and that programmability can also protect consumers from fraud and scams. The truth will depend on design choices and governance.

What a CBDC is in plain language

A CBDC is a digital form of a country’s currency issued by its central bank. Think of it as cash that lives on secure ledgers rather than in your wallet. It is different from a bank deposit, which is a liability of a commercial bank. It is also different from Bitcoin, which has no central issuer. A CBDC can be retail, used by the public, or wholesale, used by banks for settlement. It can run on a centralized database or on permissioned distributed ledgers. Programmable features are optional. Some pilots include them. Others avoid them to reduce privacy concerns.

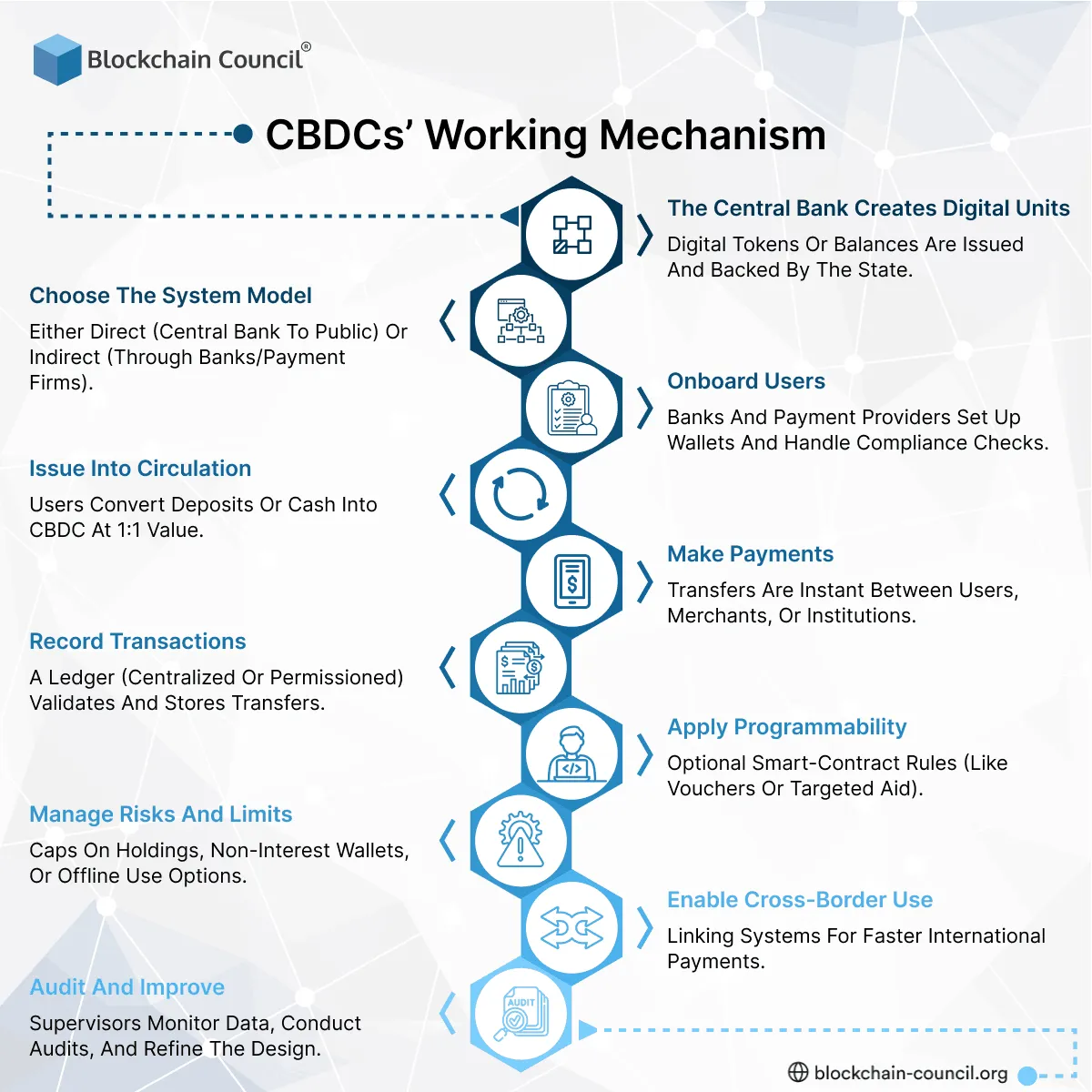

CBDCs’ Working Mechanism

- The central bank creates digital units – Digital tokens or balances are issued and backed by the state.

- Choose the system model – Either direct (central bank to public) or indirect (through banks/payment firms).

- Onboard users – Banks and payment providers set up wallets and handle compliance checks.

- Issue into circulation – Users convert deposits or cash into CBDC at 1:1 value.

- Make payments – Transfers are instant between users, merchants, or institutions.

- Record transactions – A ledger (centralized or permissioned) validates and stores transfers.

- Apply programmability – Optional smart-contract rules (like vouchers or targeted aid).

- Manage risks and limits – Caps on holdings, non-interest wallets, or offline use options.

- Enable cross-border use – Linking systems for faster international payments.

- Audit and improve – Supervisors monitor data, conduct audits, and refine the design.

Step 1. Central bank creates digital currency units

- The central bank mints digital tokens or account balances that represent national currency.

- Each unit is backed by the full faith of the state, just like cash.

- Supply and monetary policy continue to be set by the central bank.

Step 2. Choose the system model

- Two common models exist. Direct, where the central bank offers wallets to the public. Indirect, where commercial banks and payment firms distribute CBDC to users.

- Most pilots favor the indirect model to preserve the role of intermediaries and reduce central bank workload.

Step 3. Onboard users through regulated intermediaries

- Banks or authorized payment providers handle identity checks, wallet setup, and customer support.

- This keeps compliance tasks, such as KYC and AML, with the firms that already perform them.

Step 4. Issue CBDC into circulation

- Users convert bank deposits or cash into CBDC at one to one value.

- Intermediaries receive CBDC from the central bank against reserves, then credit user wallets.

Step 5. Make payments peer to peer or merchant to user

- Users pay by scanning a code, tapping a phone, or using an app.

- Transactions settle in central bank money, which reduces counterparty risk compared with card payments that settle later.

Step 6. Record and validate transactions

- A core ledger records transfers. This can be a secure centralized database or a permissioned distributed ledger with validators.

- Privacy settings vary. Some designs store only necessary data for audits. Others store more for analytics and supervision.

Step 7. Apply optional programmability

- Smart-contract style rules can attach to funds. Examples include retail vouchers, stimulus with expiration, or sector-specific subsidies.

- Jurisdictions can restrict programmability to public policy uses and ban fine-grained controls over personal spending.

Step 8. Manage risk, limits, and offline use

- To avoid draining bank deposits, wallets can have holding limits or tiered interest.

- Many pilots include offline modes so small payments work without connectivity, then sync later.

Step 9. Interoperate across borders

- Central banks test linkages so cross-border payments can clear faster and cheaper.

- Shared standards are needed for messaging, identity, and settlement.

Step 10. Audit, monitor, and improve

- Supervisors use aggregated data for fraud detection and financial stability analysis.

- Independent audits, privacy reviews, and transparency reports build public trust over time.

Where CBDC projects stand today

Dozens of countries are testing concepts. China’s digital yuan has broad trials in major cities. The European Union continues work on a digital euro with a strong focus on offline payments and privacy by design. The United States is researching wholesale and retail models through pilot collaborations. Many smaller economies explore CBDCs to improve financial inclusion and reduce remittance costs. Not every project uses programmability. Several designs prioritize cash-like privacy within legal limits, while keeping programmability for public programs such as targeted aid.

Concerns and counterpoints you should weigh

Privacy and autonomy

Critics worry that permanent ledgers create a map of everyone’s spending. Some pilots answer with privacy tiers, offline cash-like transactions, and strict access rules. The effectiveness of these safeguards will be tested in practice.

Financial stability

If people move deposits into CBDC during stress, banks could face funding pressure. Designers counter this with holding caps, non-interest wallets for retail users, and incentives to keep deposits in banks.

Innovation and competition

CBDCs may spur public rails that private wallets build on. This could open the door to cheaper payments and more competition. The key is neutral standards that let many providers compete on user experience.

Policy effectiveness

Programmable features can deliver aid faster and cut fraud. The challenge is to limit use to democratically approved programs and avoid controls that would undermine public trust.

What this means for your career and business

CBDCs, stablecoins, tokenized deposits, and Bitcoin will likely coexist. That means new jobs, new products, and new responsibilities. If you analyze markets, you will need to interpret policy moves and macro impacts on digital money. If you build products, you will work with identity, wallet security, and payment orchestration. If you operate a business, you will plan for new rails, new compliance obligations, and new ways to reach customers.

To get ready for the data side of this shift, explore the Data Science Certification. You will learn how to handle payment datasets, detect anomalies, and present evidence that supports product and policy decisions.

If you lead teams or go to market, the Marketing and Business Certification can help you translate CBDC trends into strategy. You will practice customer research, pricing, and growth planning for digital payment experiences.

Bitcoin and decentralized alternatives as a counterbalance

CBDCs are centralized by design. Bitcoin is not. That difference is why many see Bitcoin as a check on potential overreach. In practice, people may hold both. A CBDC wallet for daily use and a decentralized asset for savings or cross-border mobility. For businesses, supporting both tracks can broaden customer choice and reduce vendor lock-in. For policymakers, coexistence can encourage good behavior through competition and transparency.

Practical steps to stay ready

- Map your use cases. Identify where instant settlement and offline payments could lower your costs.

- Upgrade your literacy. Study monetary policy, digital identity, and smart contract basics.

- Build a risk plan. Document privacy controls, wallet limits, and incident response.

- Pilot responsibly. Start with sandbox integrations and clear consent flows.

- Keep options open. Design systems that can support CBDC, stablecoins, and card rails side by side.

Conclusion

Calling CBDCs the closing of the “1984 loop” captures a real fear about power and privacy. Yet outcomes are not fixed. Design, law, and public oversight will shape what CBDCs become. The best position is an informed one. Learn how CBDCs work, track pilot designs, and build skills that let you evaluate technology on its merits.