HMRC’s New Crypto Tax Rules in the UK

Starting January 1, 2026, HMRC will begin enforcing stricter crypto tax rules in the UK. The changes will require crypto platforms to share personal and transaction data directly with HMRC. Investors and traders will face tighter reporting duties, reduced tax-free allowances, and new ways their activities are tracked. In simple terms — if you use, trade, or earn from crypto in the UK, you’ll now have to treat it like any other taxable financial activity.

This guide explains what’s changing, how it affects different users, and what you should do to stay compliant and avoid penalties.

What Are the New HMRC Crypto Tax Rules?

The updated rules are part of the UK’s adoption of the OECD’s crypto-Asset Reporting Framework (CARF). This aims to make crypto tax reporting as clear and traceable as traditional finance.

Personal Details Must Be Shared

From 2026, crypto platforms must collect and share user data with HMRC. That includes:

- Full name

- Date of birth

- Home address

- National Insurance number or tax ID (for foreign users)

Companies will need to submit business identity details too.

Platforms Must Report All Transactions

crypto platforms will report every trade or transfer linked to a UK taxpayer. This includes the type of asset, transaction amount, number of units, and the nature of the transaction (buy, sell, receive, send, etc.).

If a platform fails to report properly, HMRC can fine them £300 per affected user.

What This Means for Crypto Users in the UK

Whether you’re a casual trader, long-term holder, or DeFi enthusiast — you’ll need to pay closer attention to taxes. HMRC will now know exactly what you’ve bought, sold, and earned.

Who Is Affected?

- Individual traders

- Investors holding assets long-term

- DeFi users earning staking or yield rewards

- Businesses transacting with crypto

- NFT buyers and sellers

Even small one-time profits may trigger reporting requirements.

What’s Taxed?

- Capital Gains: When you sell or swap crypto and make a profit.

- Income Tax: If you earn crypto via mining, staking, airdrops, or work payments.

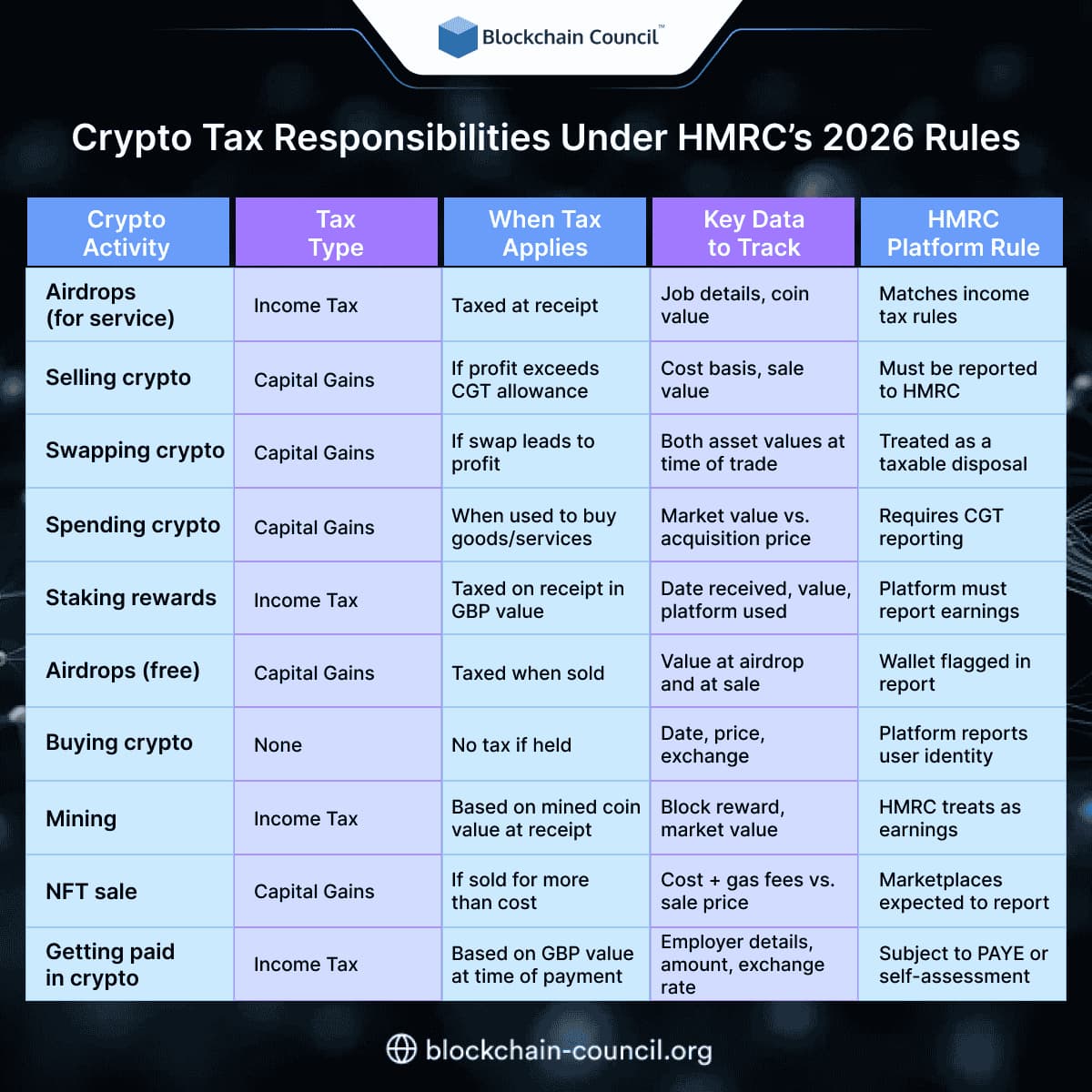

Crypto Tax Responsibilities Under HMRC’s 2026 Rules

That means even small profits from crypto will be taxable. If you sell BTC, ETH, or any other crypto at a profit over £3,000, you’ll need to declare and pay CGT.

How Are Capital Gains Calculated?

Let’s say you bought 2 ETH at £1,000 each and later sold both at £2,000 each.

- Cost: £2,000

- Sale price: £4,000

- Gain: £2,000

If your total gains from all assets (crypto, stocks, property) exceed £3,000 in the tax year, you owe tax on the surplus.

Note: Gains from residential property are taxed at a slightly higher rate. Crypto is treated like other financial assets.

Income Tax on Crypto Earnings

If you’re earning crypto through staking, mining, or DeFi protocols, it may count as income.

You’ll be taxed based on the GBP value of the coins at the time you receive them — not when you sell them.

Common Sources of Taxable Crypto Income

- Staking rewards (e.g. from Ethereum or Solana)

- Airdrops from projects

- Liquidity pool earnings

- Getting paid in crypto

Depending on your total income, tax rates range from 20% to 45%.

For those using AI tools to automate crypto trading or DeFi strategies, this is a good time to track every transaction using a tax-friendly tool — or even learn deeper insights with a Data Science Certification to manage analytics and reporting.

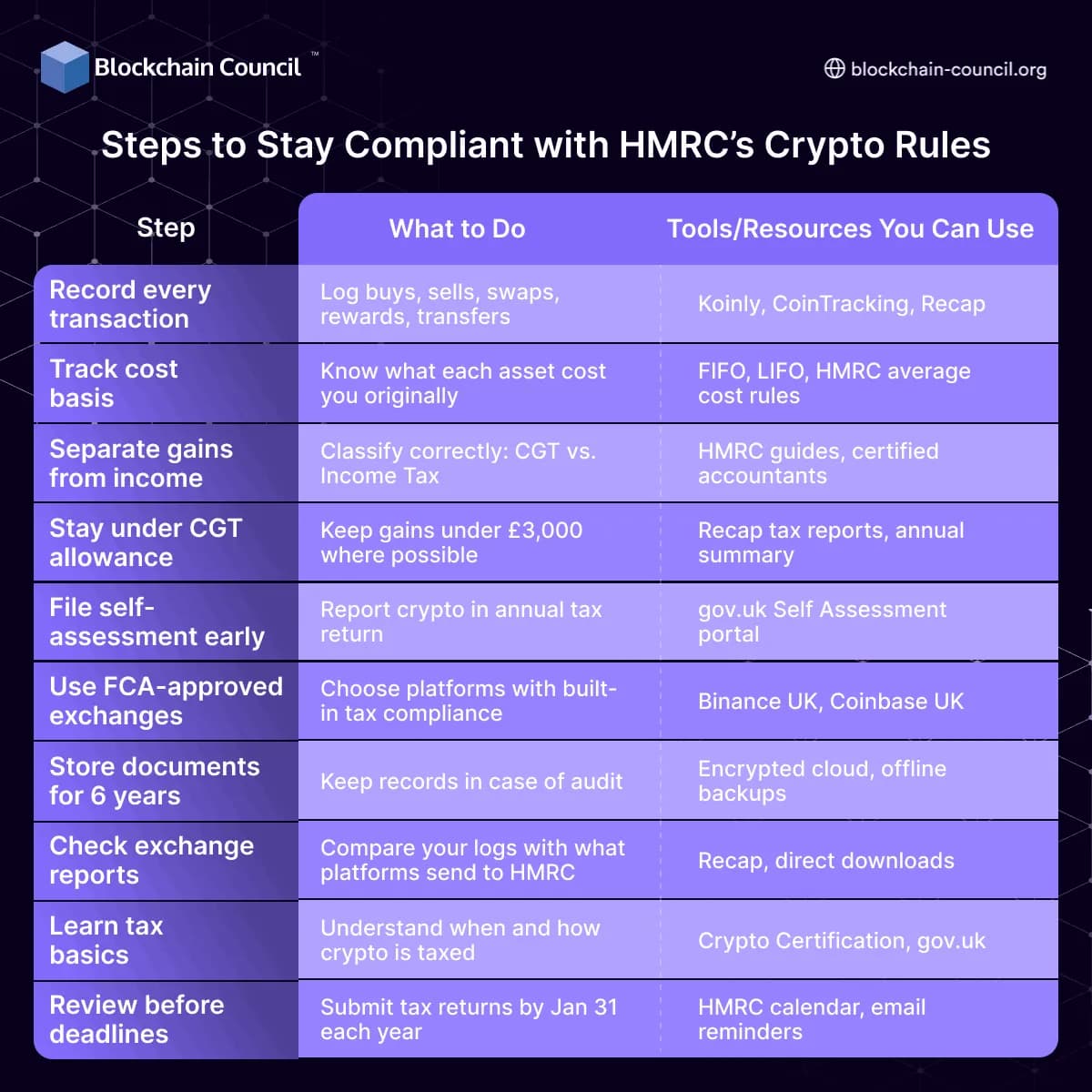

How to Stay Compliant?

Keeping records is more important than ever. If HMRC has your data from the platform and your return doesn’t match — penalties could follow.

Steps to Stay Compliant with HMRC’s Crypto Rules

To Stay Compliant, You Should:

- Use FCA-registered exchanges

- Record every buy, sell, transfer, and airdrop

- Track cost basis for each coin

- Use crypto tax software or spreadsheets

- File your Self Assessment return accurately

- Pay any taxes owed before the January 31 deadline

Learning how tax rules affect trading strategies is key if you want to scale a crypto project or work in crypto finance. Consider a Crypto Certification to deepen your knowledge of regulations, tokenomics, and blockchain reporting.

And if you’re turning your trading or DeFi experience into a business, a Marketing and Business Certification will help you understand how to operate in a regulated environment.

Timeline of Changes and Deadlines

| Date | Rule or Requirement Introduced |

| Jan 2024 | CGT allowance cut to £3,000 |

| Jan 2025 | New crypto income reporting rules added |

| Jan 2026 | HMRC gains full data-reporting access from platforms |

| Jan 31 each year | Self Assessment deadline (for prior tax year) |

Crypto tax isn’t optional. These rules mean HMRC will know what you owe — even if you don’t report it. You need to stay ahead, stay compliant, and make crypto part of your financial plan.

Final Thoughts

HMRC’s new crypto tax rules aren’t just another policy update. They’re a shift toward treating crypto like every other financial asset — taxable, reportable, and transparent.

For UK users, that means no more flying under the radar. Every coin, every swap, every reward will be part of your tax file. But it also means greater clarity and a more mature crypto ecosystem.

With the right tools and knowledge, these new rules don’t have to be a burden. They’re a signal that crypto is growing up — and that investors, traders, and builders need to grow with it.

Related Articles

View All

Cryptocurrency

Common Crypto Tax Mistakes and How to Avoid Them in 2025

Avoid common crypto tax mistakes with better records, correct cost basis, income classification, and preparation for Form 1099-DA reporting.

Cryptocurrency

Crypto Tax Reporting Checklist: Transactions, Records, and Forms to Track

Use this crypto tax reporting checklist to track taxable transactions, records, and IRS forms for sales, swaps, staking, mining, gifts, and income.

Cryptocurrency

Crypto Tax Basics: What Beginners Need to Know Before Filing

Learn crypto tax basics before filing, including taxable events, cost basis, 1099-DA reporting, staking income, capital gains, and beginner record-keeping steps.

Trending Articles

Top 5 DeFi Platforms

Explore the leading decentralized finance platforms and what makes each one unique in the evolving DeFi landscape.

How Blockchain Secures AI Data

Understand how blockchain technology is being applied to protect the integrity and security of AI training data.

What is AWS? A Beginner's Guide to Cloud Computing

Everything you need to know about Amazon Web Services, cloud computing fundamentals, and career opportunities.